{kind=link}

Islamic higher education responds to globalization in ASEAN (Choi, 2010). SIHE (the State Islamic University) definitely constructs more extended in any program taken. It serves inter-disciplinary and trans-disciplinary program such economics, politic, public relation even accounting program at which Islamic higher education goes international level (Wit, 2020). Shortly SIHE broaden in term of developing the program as flexible as how they construct the financial management for public. Structurally SIHE (Dhont, 2016) is under the MORA, from the aspect of regulation (Pintrich, 2000) and supervision must submit to the authority of MORA and Ministry of research and higher education since it develops many programs of the faculty and general program such sciences and technologies (Ahmadi, 2005 ).

In accordance with article 1 point 23. Law Number 1 of 2004 concerning The State Treasury states that the Public Service Agency is an agency in government environment formed to provide services to society in the form of providing goods and / or services that are sold without prioritizing profit-seeking in carrying out its activities based on principles of efficiency and productivity (Lukens-bull, 2016). Even SIHE comes to WCU (world Class University) to compete in the international education that the way to how SIHE(s) have to construct strategies, plan, target and program to international-standard recognition (Salmi, 2009). This idea will be needed high cost and funding to be competitive amid globalization and development growth Islamic university as BLU (Abdullah, 2017). SIHE recently face against the quality improvement to which ministry of religious affairs and ministry of monetary will monitor anytime to assess the financial management and good quality services to public (Bahri, 2012).

This concept adopts the emerging paradigm in public sector management, namely the New Public Management (NPM) approach where the main core of this approach is to transform the entrepreneurial spirit into the public sector (Koe, 2018) by naming the concept of his approach as reinventing government (David Osborne, 1992). The entrepreneurial spirit is that the Public Service Agency can implement healthy business practices by conducting financial management efficiently, effectively, professionally, accountable, and transparently (Hefner, 2008), by making changes from traditional budgeting to budgeting based on government performance. A financial management constitutes the methodology that organization uses and applies also system budgeting system of operational at work mobilization (Republik Indonesia. Peraturan Pemerintah Republik Indonesia Nomor 23 Tahun, 2005).

Government ensure and control its incomes, expenses, and asserts with the objective maximizing sustainability. It processes and procedures will be controlled and accountability under the authority of ministry of monetary. These views will be analysed deeply on how this research question come from. SIHE(s) financial managements will be discussed comprehensively as the response of public transparencies (Sri Sumarni A. D., 2015). The transparencies becomes integral responsibilities (Tan, 2012). The assessment and evaluation reflect to public consume to explore further, moreover the services quality indicated works performance of SIHE(s) financial management. The competitive approaches become the ideas and reflect work target and obligated work performance indication to MORA.

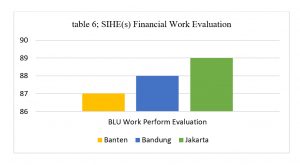

The control of SIHE budgeting under External Board Supervision (DEWAS) come to evaluate the consistency of upgrading annual financial work perform. Dewas contributed the assessment to which State Islamic University (UIN-Public Agency Institution) evaluation (Syihabuddin, 2015). Progressive budgeting-based programs increased services to the public. The progress to better quality in both academic services and non-academic (financial services) end to high quality work performance (Hefner, 2008). The performances response the transparency of institutional public services (David Osborne, 1992). In case, SIHE as public service in terms of financial management to serve public opinion for the users and government. Though the research of the idea rarely found in the Ministry of Religious Affairs of Indonesia (Abdullah, 2017). Due to the main services of non-profitable (Goodman, 2011) bodies under the MORA (Ministry of Religious Affairs), SIHE(s) are strongly recommended to display the annual progress of services improvements. The SIHE’s improvements constitute a proven works performance as recorded to prime documents of reports. The reports describe such financial management; active BLU incomes and government budgeting incomes (Sri Sumarni A. D., 2015) that reflect to prior to academic and non-academic services. The SIHE performance deeply receivable to public affairs (Lukens-Bull R. A., 2013), (Davis, 2013). In term of this, (Laws number 17/2003, on National Monetary, 2003), (Abdullah, 2017).

Supervision as the integral part of the ongoing proses of public agency institution financial management. SIHE’s integrated supervision must maintain the quality of performance. How to strive for its resources, its capacity, and most importantly its supervisory competence. There must be a change in mind-set from a conventional one to a new paradigm. The importance of synergistic oversight that will produce comprehensive information that will greatly benefit strategic and substantive decision-making. In addition, synergistic supervision will encourage effective and efficient supervision and consider risks and priorities of concern at a more strategic level.

SIHEs’ supervision, external board supervision (DEWAS), controls management of cost running and existing cost as idle cash. Controlling and evaluating of SIHE financial management indicate work performance and accountability of the progress program annually.

Finally, the financial statements of the public service institution work unit are expected to produce principal financial statements for the purposes of accountability, management, and transparency, fixed asset reports for the purposes of fixed asset management, as well as generating unit cost information per unit of service, performance liability or other information for managerial purposes. Role of external supervision board (DEWAS) and external public accounting are most integrated parts in evaluating SIHE work performance.

Performance measurement is one of the important elements of the system control of the management of an organization, which can be used for controlling those activities. Each activity must be measurable in order to perform can be known the level of efficiency and effectiveness. Performance measurement is the process of recording and measuring achievements implementation of activities in the direction of mission accomplishment (mission accomplish) through the results displayed are in the form of products, services or processes. Process performance measurement is intended to assess the achievement of each indicator performance to provide an overview of successes and achievements goals and objectives. The process of measuring the performance of an organization should be use comprehensive performance indicators that contains both financial and non-financial indicators, so necessary a performance measurement system that can accommodate indicators the comprehensive evaluation (Contributor: As’ari and Hidayatullah @uinsmhbanten)